Marketing Committee Q&A

Question (1/19/21): Does anyone have a joint marketing agreement that they use with partners they would care to share?

- No marketing agreement. Contracts come from the vendor and are negotiated from there.

Question (1/19/21): Who everyone is using for the their customer email program. Constant Contact? MailChimp? Something else?And has anyone had any issues with customers raising concerns about the emails they receive because the links shown in the rollover do not look like the bank’s URL? We are using Constant Contact and they add unique coding to the hyperlinks to use for tracking purposes and a customer became suspicious that it was a Phishing email. Just wondering if this a common issue or if there are other options out there that don’t create this concern.

- GetResponse. There are pros and cons. The price is great but there are limitations. I am hoping to add Pardot marketing automation onto our instance of Salesforce and start pushing out email campaigns through that

- Salesforce and are working on the integration with our new core – FIS Horizon, and plan to use Pardot as well. It should be fully integrated. I don’t know if there will be an issue with the URLs.

- Constant Contact – Issue with delivery – so many emails don’t reach the recipient even with a valid email. It doesn’t support the ability to send informational and marketing emails with no opt out capability.

- Constant Contact with no complaints from customers about the links. A new CRM that is core integrated will eliminate the need for Constant Contact.

- Constant Contact for one off emails and moving to SendGrid for automatic emails. There is automation with the core to auto send emails based on certain user “triggers”. SendGrid is good for automation, Constant Contact good for design. We put UTM codes in all links for tracking purposes.

- Use KASASA. In addition to KASASA pushing out emails, we use Constant Contact and have been pleased with our email campaign performance. To date there have not been any complaints about coded urls.

Question (1/25/21): What are you doing with your Annual Report this year? Are you printing it or creating a digital annual report instead?

- We will still print our annual report this year but each year we reduce the quantity and post a digital copy on our investor relations website. This year (and last year) we removed the marketing piece—less stories, text and photos and focus on the financials.

- We are still producing a printed Annual Report however we printed significantly less last year so I feel that will apply for this year as well. We have added the pdf version of our annual report to our website for the past few years.

- In 2017, we cut our Annual Report marketing piece down to 1 page (front and back), which includes a letter from our chairman and financial highlights. We print a small run and also post it on our investor relations website. Last year, we bound the marketing piece and 10-k together with a nice color cover. There is continued debate on how many we should mail out to shareholders, but last year we were forced by the pandemic to provide it digitally to everyone except for those who contacted our transfer agent to request a printed copy.

- For the second year in a row, we will be producing an Annual Report that will be distributed digitally.

- We are both producing a print version and a digital version (which lives on our website) – we did this last year and it worked well. We’ll reduce the numbers being printed but not significantly.

- For the past several years we have posted a pdf on our website, as well as printed hard copies. Our shareholders and customers like the full-on version we develop each year, so we’ll continue with the format. We had great success distributing our 2021 calendar through the drive-ups. If our lobbies are still unavailable to walk-in traffic when the report publishes, we will probably do the same with the hard copies we have for customers and guests. We also distribute through the welcome centers in our markets and take a few copies to Chambers of Commerce and hospital waiting rooms. They’re a great introduction to the bank. We may not print as many this year, but we will print them.

- Both – it has a marketing element and we print it as well as make it available digitally, but have significantly reduced the extra quantities.

- In the past we have created the traditional printed piece featuring our clients and lines of business and included a pocket in the back for the financials. I usually overprint to keep 300 on hand for business development and other community outreach and another 300 are mailed to our shareholders in advance of the annual meeting. Even before 2020, its usage in print had gone down and I found we had too many extras that were thrown away. With COVID and the shift towards much more digital access, we decided this year to create the report as an interactive micro site linking to content throughout our website, expanding on existing customer stories as it relates to the support needed through PPP, as well as highlighting our digital capabilities from our core conversion last year. We will print a small quantity for the shareholders’ mailing and for marketing purposes, provide links to the micro site in our communications.

Question (1/25/21): Are you using a scheduling tool or partner to manage the branch appointment process?

- No, we currently aren’t using a scheduling tool however I have shared with our teams the availability for us to do this via Facebook and Google My Business. Has anyone considered those two options?

- We just kicked off this project with Kronos, so we plan to have an online appointment scheduling tool soon. Their solution also includes a component called Lobby Tracker which helps monitor the execution of appointments and streamline the overall process.

- We do not use a scheduling tool at this time. The branch sets the appointments.

- We are not using a scheduling tool or partner – we do have links to forms on our website where folks can request appointments with various specialists. Our branches are open so no official appointments are needed for regular entry.

- Up to now, we’ve encouraged customers to call their branch direct. However, we are looking into incorporating a scheduling tool on the website.

- Yes, we launched Kronos a couple weeks ago and its going great. We haven’t promoted it but customers have found it via the link on our website.

- We are not using a scheduling tool. All of our branch lobbies are open for walk-in assistance.

Question (2/1/21) : February is Black History Month. I would love to see what other banks do for this celebration. Do you run any ads, special social media posts, or any other type of marketing efforts?

- The past two years, FNB has had Black History month spotlights throughout February on our Facebook page, and those have been some of the most highly viewed posts we’ve had for our social media presence, full stop. I initially kept the posts focused on figures local to our region, like Anne and Chauncey Spencer and Dr. Robert Johnson (in order: a renowned poet, the founder of the Tuskegee Airmen, and the coach of Arthur Ashe and Althea Gibson), as well as Maggie Lena Walker (banking pioneer). The second year, I focused on the Harlem Hellfighters, HBCUs, and Katherine Johnson, NASA legend. For Anne and her son Chauncey, I actually interviewed Shaun Spencer, Chauncey’s daughter. She gave me a copy of some of her grandmother’s poems, as well as family photos to share on our page. I also interviewed Dr. Johnson’s surviving daughter for some firsthand insight. For the second year, in addition to the spotlights, I shared local museums and tours tied into Black History. This year, I’m thinking of Barbara Johns, since this is the 70th anniversary of the historic protest she led working towards integrating schools, and that gives way to Ruby Bridges, my second spotlight. That’s my very long-winded way of saying yes, we do.

- We are planning a some social media posts to highlight Black History Month.

- We have social media posts highlighting notables during Black History Month. With Barbara Johns being from Farmville and some of her family still very much present, as well as my Marketing Officer being on the Board at the R.R. Moton Museum, we have opportunities to add the local interest we believe are important to include. We replicate some of these individuals on our in-branch video monitors, as well.

Question (2/4/21): Does your bank offer contactless debit cards? Can you tell me if you did a mass re-issue of all cards? Or issued contactless cards just as the old card expired? If you do offer them, can you share your reasons or thought process for why you decided to offer them?

- We do not have any current plans to offer contactless debit cards. This is due to a lack of customer interest, low number of merchants taking contactless and the higher cost of plastic. Also, we prefer to focus on digital wallets as a form of contactless payments.

- We are not offering contactless payment except through the digital wallet. We’ve had pretty good success with that for now.

- We just started offering contactless debit cards and have decided to switch cards over as they expire instead of a mass re-issue. The goal was to offer our customers more contactless payment options (in addition to mobile wallets) given the pandemic circumstances. In our area we are seeing increasing demand for this option, but not quite enough for us to justify the cost of a mass reissue.

- We began issuing them as part of our system to FIS/Horizon – shows we can offer similar services larger banks do. Not knowing a pandemic was looming when we established the scope of services in the conversion, we knew it was newer technology and this was a good time to introduce. We only have promoted them softly on our website and in other materials that list our services. We did not do a mass reissuance; customers will receive the new card upon expiration. We are working on instant issue too, and those cards will also be contactless. However, our ATMs are not yet programmed for our customers to use. Working on that this year. I think our customers need a tutorial on the functionality so I plan to do more direct promotion using our email marketing (whenever I can get it up and going).

- We would like to offer contactless, but I believe JHA does not have things ready for us to be able to offer it with our debit cards but as soon as they do, we’ll be adopting.

- We are offering contactless payment via mobile wallet and have been promoting at least once a month. So far I have not heard of us moving to update our debit cards to contactless to date. I do know our credit cards are issuing contactless for new cards.

Question (3/17/21): Do you post job openings to your social media? If so, how successful have you been with finding good candidates?

- We post a generic “we’re hiring” advertisement and direct them to our website. It has provided positive results for us as our employees start to share it as well.

- We use LinkedIn but not Facebook

- We do not post openings on social media, but we have found great success in boosting our Indeed job postings. We do anywhere from $5 – $50 a day depending on the urgency and have seen an upward of 250 applications daily. We do encourage questions to filter down applicants, as when you boost the job postings you will get a lot of responses.

- We post our job openings on LinkedIn only.

- We post on Facebook, Twitter, Instagram, and Linked In. We’ve heard from HR anecdotal stories that some have learned about positions that way.

- Currently we only post on Indeed. I have been lobbying my HR team to post positions on our website so we can link from LinkedIn. I would think on social it would help drive more traffic to the website.

- We post on Facebook & LinkedIn (as a news feed post & job posting). We have seen an increase in applicants and have hired employees that have seen the job(s) on social. For us, it’s helpful when employees share it, so people in the community or circles of influence see it & may point someone in our direction.

- We post on FB and get lots of applications. Also, Indeed and on our website.

- We tried posting job openings on all our social media feeds (Facebook, LinkedIn and Twitter) briefly but the candidate quality wasn’t quite what we were looking for. Now we only use LinkedIn for job postings.

- We do post to our social media channels (Facebook, LinkedIn, Twitter) and our applicant system automatically posts to some free FB job site. We’ve seen no results from there. We get almost all our candidates from Indeed – another source that our applicant system posts to.

- We have posted a few job openings on LinkedIn however I am not sure if any applicants from that channel were hired.

- We post positions as “Come work with us” or “We’re Hiring” on Facebook and LinkedIn, as well as job listings on Indeed. Like some of you, the social media posts are liked and shared by our employees and followers who share with their friends. Our HR Director tells me our referral fee for employees is our most successful recruiting tool.

- We post job both general we’re hiring posts and specific job listing posts on LinkedIn, Facebook, Instagram, and Twitter. It’s been effective and also encourages our employees share it and help with recruiting.

Question (4/7/21): What are your bank’s plans for Juneteenth this year especially since the holiday falls on a Saturday?

- We will be posting a few things on our social channels leading up to the day, and then a post on Juneteenth itself. There’s lots of great resources (for teachers, but still) here: https://www.weareteachers.com/teaching-juneteenth/

- We will be closing our branches on that Saturday.

- We will be closing our branches that Saturday. We added it to our calendar in January and the teams were very happy to see we are observing the holiday. We will also plan to run some social media posts. And looking forward to hearing what others are planning.

- There are several holidays observed in our communities that the bank does not formally celebrate since they are not federal holidays. Juneteenth is one of those. While we don’t formally celebrate Juneteenth, because of its significance to a segment of our employees and the importance for all of us to be aware, our president will send out a bank wide awareness email informing our employees of the day’s origin and encouraging our employees to be mindful of its significance.

- All of our locations will be closing at 2pm Friday 6/18 and the branches that have Saturday hours will be closed Saturday.

- We are closed on Saturdays. We are still finalizing our plans for honoring Juneteenth.

- We are not open on Saturday. We will have some social media posts about Juneteenth.

- We will acknowledge Juneteenth through our social media outlets as we did last year. We are not planning to close as we follow the federal calendar.

- We’re not open on Saturdays, but if it fell on a business day we would most likely be closing or closing early. We will also be posting on social media to help educate about and celebrate it.

- Our branches that are open on Saturdays will be closed. We will most likely do a social media post as well.

- We will be posting on social some educational material about the day and its significance, then a celebratory post the day of. This site has some great resources: https://blog.tcea.org/digital-resources-juneteenth/.

- We currently do not have any plans for the day.

Question (4/27/21): I’m curious to know what others are doing in response to mandating/encouraging the vaccine. What have they done to promote confidence? Any timelines set?

- That has been a topic of discussion with us as well. We are taking the stance of “encouraging” our team to get vaccinated by providing helpful vaccination information, vaccination times, and facts regarding the spread of the virus. We are not trying to “scare” anybody, but more keep them informed and allow them to get vaccinated if they would like. We are planning on opening up our lobbies soon (which have not been open since COVID), and are encouraging everybody to get their shots before hand. Also stating, if they choose not to get vaccinated that is fine, but letting them know the greater risk they are opening themselves up to.

-

Our CEO and CHRO send out regular updates on the vaccination status of the bank as a whole, and employees who know about extra doses or open slots at vaccination sites are encouraged to share that information with their building. We’re also looking into getting some onsite vaccinations set up.

-

Our president sent out a memo last week encouraging people to take the vaccine, but has left it up to personal choice as to whether they do. He and our bank leadership team have all gotten our vaccines. Our employees are being given time off to take the vaccine and to accommodate any reactions without having to dig into their PTO. No timelines here.

-

We are back to 50% capacity in the office, which means 3 people can be in my office suite at a time! Plus ½ a person, which is what I feel like some days. We secured vaccine appointments at a local site that ended up opening to the public two weeks ago. Our HR and Wellness teams advocated for people to take time from work to get the vaccine if needed. Our homepage on SharePoint has a link to our Vaccine Resources page, which includes CDC information on the vaccine, resources to make appointments, and a library of our internal communications.

-

We opened our branch lobbies on April 12 and remote workers are starting to move back into the offices, while some have maintained a hybrid schedule. We also have published a lot of information about vaccines on our website, including where across our footprint people can get one. We’ve encouraged people to get the vaccine in our bank-wide meetings and other communications, but there is no mandate.

-

We are also encouraging employees to get the shot, but not mandating it. Our HR team has been sending bi-weekly vaccine tips out through our intranet with vaccine information and resources/locations to make appointments. Most of our management has gotten their vaccine and getting your vaccine also enters you into a company drawing for some nice prizes (ie. Roomba, SmartTV, etc.). Our lobbies are currently open with a doorbell system and we’re anticipating reopening them fully soon. We’re at about 50% in the office now and we’ve been discussing additional phases of bringing the rest of our employees back – probably phase 1 in July and phase 2 by September-ish. We are also discussing with HR on officially reclassifying our job positions as either (i) always in office, (ii) fully remote, or (ii) hybrid with guidelines.

Question (6/17/21): Have any of you used Kadince (community involvement software)? If so, how well did it work?

-

We took a quick look at Kadince last year. I liked what they had to offer – sounded like a quality product. The pricing as I recall for the donations, volunteer hours piece was coming in around $5000-8,000 one time fees plus an annual subscription around $10,000. As I remember, my takeaway was that it didn’t make sense unless we coordinated with our Compliance team to include the CRA portion of what they can track. And for us, it was a bit steep for the volume we currently deal with. We currently aren’t tracking volunteer hours that our employees do outside of work-related activity. So I saw potential depending on the direction our bank takes but we didn’t take it further at that time. Their pricing may be bank/program specific so you may face a completely different scenario.

-

That aligns with what our Community Engagement Manager was presented in January. We shelved it for the time being because of timing issues and questions we need to consider about how it will impact our connection with our non-profit partners. Really need to think through it but did not have the bandwidth to give proper consideration at the time.

Question (6/17/21): We are considering modifications to our dress code. Would anyone be willing to share your bank’s dress code?

Below is our dress code & policy on tattoos. We’re pretty lax. We wear jeans on Fridays & Saturdays. Our operations center (call center, dep ops, IT, loan servicing) are in a separate, non-customer building, and can wear jeans daily. You may wear business attire or business casual attire as long as you follow these guidelines.

BUSINESS ATTIRE:

- For men, business attire includes a long-sleeved dress shirt, tie, sport coat worn with dress trousers (not khakis) and dress shoes.

- For women, business attire includes pantsuits, businesslike dresses, coordinated dressy separates worn with or without a blazer, and closed-toe shoes.

BUSINESS CASUAL:

- Appropriate - leggings with thigh length jacket or top, suit pants, khakis or corduroys, capris, dress slacks, casual slacks, polos, golf shirts, oxford shirts, company logo wear, short sleeve blouses or shirts, blazers, jackets, dressy sleeveless shirts, dresses, jumpsuits, boating or deck shoes, casual low heel shoes, sandals, open back shoes (mules), open toe dress shoes, dressy boots.

- Inappropriate – sweatpants, uncovered leggings or exercise wear, shorts, ripped jeans, t-shirts, beachwear, exercise wear, crop tops, off the shoulder tops, flip flops, tennis shoes.

Policy on jewelry and tattoos: The company recognizes that personal appearance is an important element of self-expression and strives not to control or dictate appropriate employee appearance, specifically with regard to jewelry or tattoos worn as a matter of personal choice. In keeping with this approach, we allow reasonable self-expression through personal appearance, unless a) it conflicts with an employee’s ability to perform his or her position effectively or with his or her specific work environment, or b) it is regarded as offensive or harassing toward co-workers or others with whom we conduct business and has contact with employees.

This is a communication we sent out to all employees last week. Over the past 14 months, we veered away from adhering to our dress code policy in effort to make life a little bit more comfortable in the midst of a really difficult year. As we settle back into our new normal on September 7th, we will reinstate the dress code with one amendment; now every Friday is a Jeans Friday! I have attached a copy of the current dress code from our Employee Handbook. This will be updated to reflect the addition of Jeans Friday in the near future, and it will be published along with our 2021 Handbook update. Customer facing employees should already be abiding by this policy. Please remember, although we are not formally reinstating the policy until September 7th the following items are never appropriate for the workplace:

- shorts, capris, cargo style, cropped pants, leggings

- t-shirts, tank tops, low cut tops, spaghetti straps, midriff-baring tops, halter dresses, sundresses

- flip flops, beach shoes, thonged or casual sandals, construction or hunting boots, boat shoes

- athletic wear

- ripped, torn or frayed clothing, sheer or tight clothing

- visible tattoos or body art, extreme hairstyles, hair color not generally found in nature, piercings other than earlobes, any gauging, and unkempt facial hair. **This list is not exhaustive**

This is from our staff handbook

8.24 –DRESS CODE

Employees are expected to dress in business casual attire unless the day’s tasks require otherwise (i.e. Board meetings, client meetings, business lunches or events) Employees must always present a clean, well-groomed professional appearance, with limited visible body piercing or tattoos. Clean clothing should be pressed, free of holes, tears, or other signs of wear. Makeup, hair color and nail color should be conservative. Clothing with offensive or inappropriate designs or stamps are not allowed. Clothing should not be too revealing. Clothing and grooming styles dictated by religion or ethnicity are exempt. Footwear: casual walking shoes, boots, flat or dress heels Word of caution: inappropriate footwear that exposes the feet or toes could present potential for injury in the workplace (i.e. dropped items, injury from chairs with wheels) Jewelry and Accessories: All should be in good taste. Less is more. Perfume and Cologne: Fragrance should be worn with restraint as some people are allergic to the chemicals in perfumes and colognes. Avoid:

- o Denim jeans or clothing made with jean material

- o Leggings that are not appropriately accessorized with proper top length. Pant-type and solid color leggings are allowable.

- o T-shirts or sweatshirts

- o Logo wear, other than bank logo. Discreet school logos or clothing brands are acceptable.

- o Athletic wear

o Tennis shoes (acceptable with management approval based on physical comfort) or flip-flops o Clothing that is too tight or too loose. o Hats, unless the head cover is required for religious purposes or to honor cultural tradition If attire fails to meet these standards as determined by the employee’s manager or HR, the employee in violation is expected to immediately correct the issue. This may include having to leave work to change clothes. This time will not be compensable. Repeated violations or violations that have major repercussions may result in disciplinary action being taken up to and including termination.

I ran this question past our HR Director and Here’s our current dress code: Employee appearance should be clean, neat, and appropriate at all times. Extremes of any style are not permitted. Specific guidelines for appropriate attire Monday through Thursday are as follows: Dress shirts and dress blouses with coordinated dress pants/skirts. Dresses which are appropriate in length and cover the shoulder and back may also be worn. Business suits and ties are optional but should be worn when a more professional attire is appropriate –ie. meeting a client or attending an event outside the bank. Prohibited Clothing – Because of changing styles and designs, it is not possible to list all types of appropriate or inappropriate attire. The governing rule must be whether, in the opinion of management, the employee presents a professional appearance consistent with business needs. The following clothing does not present a business appearance and is prohibited: Denim or corduroy jeans or jean-type apparel (dark denim dresses/skirts allowed); Casual pants, ex. dockers; (Except on Fridays) Tennis shoes, western boots and moccasins; Shorts; short-or mini-length skirts; jumpsuits; Sundresses (unless bare back and/or bare arms are covered by a jacket/sweater), halter tops, tube tops; Tank tops, cropped tops, T-shirts, sweat shirts, sweat suits or jogging suits; Mid-lower calf-length (Capri) pants, tights or leggings (unless worn underneath appropriate length dress/skirt) Sexually-provocative or revealing clothing. For our back-office employees not in retail, potentially customer-facing offices, the dress code is more relaxed, though business casual is always appropriate.

Question (7/8/21): Does your bank have a call center (either bank-staffed or outsourced)? If so, who does that department report to? And, if it is in-house, how many employees staff the call center?

- We have an in-house call center with typically 4-5 employees (1 is a manager of the CCC). The call center is considered a “branch” and reports to a regional manager and director of retail.

- We have an internal Customer Care Team under our Director of Operations & Technology and Operations Manager. The Team is a staff of 7.

-

We have a call center – referred to as the eClient Services Center. The team mainly handles online banking/mobile and treasury inquiries and issues. Reports up to our Treasury Services team due to the scope of their responsibilities. It is bank-staff and the team consists of 2 associates, a manager and the manger reports up to the SVP of Treasury. We rolled this service out just before our system conversion to FIS at the end of 2019. Very valuable during that time. The responsibilities may eventually evolve to include all customer inquires, but we are not there yet and they may require another team member to be added.

-

We’ve got eight employees who report to our Customer Support Supervisor, under the Ops umbrella. After hours, we have an automated messaging system with the same voiceover as our hold line. On weekends, we have an outsourced group just for debit card issues.

-

We have an in-house Contact Center team of 6 people who are available during business hours and handle all types of customer calls. After hours, customers are routed to telephone banking services or after hours debit card support through FIS. They report to our Digital Services Officer who reports to our COO. (Our Digital Services officer also oversees another team who handle our ACHs, Wires, Treasury payments/servicing, etc.)

-

We have 13 folks in our Contact Center in Alexandria reporting to our head of Operations. They respond to all calls to the Bank – we have very little direct dial. So they perform all functions and customer support. They work M-F, 8 am – 7 pm and Saturday, 8 am -5 pm.

-

We have 3 in-house Customer Care Specialists. They report directly to the Deposit Operations Manager, who reports to the Operations Officer (who reports to the CEO)

-

We currently have a director and 19 employees. We are now operating 24/7 so obviously many of these employees work different shifts. The team reports to our head of Retail Operations and the responsibilities include processing online account openings for retail and business, password resets and login problems, ordering checks (if needed) and all customer inquiries.

-

We have an internal support center of four that handles online account opening as well as other general questions as needed. We also partner with Jack Henry’s call center, which is both during bank hours and before/after hours. That hasn’t been the best solution so we are considering bringing everything in house. Our internal support center and call center operations report up to our CIO.

-

We have a customer care center consisting of 85 teammates in 4 different locations across VA, 75 are actually call center teammates that answer phone, chat and online questions. A smaller group consist of teammates that answer any social media questions and address any positive or negative posts that may appear. Online account opening goes thru our CCC as well for the review process and support as those people open online. The senior manager of this entire department we call” Customer Experience Team” reports directly to our president.

-

We also have an internal Customer Care team. It consists of 6 employees. 5 of the employees report to the Customer Care Manager & she reports directly to our SVP/ Retail Services. In additional to answering customer calls & online questions, they are responsible for our online account opening (loan and consumer) too.

-

Question (7/22/21): Do you have a company that monitors your website for ADA compliance and if so, can you share the company? Would anyone share their “Social Media Procedures”?

-

We do not have a company that monitors for ADA Compliance. I would think this could be part of a webhost service, but I don’t think our webhost offers it and if they do they have never contacted me. I will be switching webhost companies next year – leaving Banno/ProfitStars/Jack Henry. Would be interested in knowing if others work with a separate company of it’s part of the webhost contract. I don’t have social media procedures, per se, but I am in the process of updating our policy to include more details on the compliance/risk management of the program. Happy to share with everyone once it’s been approved by our board in late August.

-

We use NCR/Digital Insight for web hosting (and other things). A few years ago, we had them clean up our website in response to reports that banks were being sued for non-ADA compliance while the industry had not yet received any definitive guidance. Since then we use SiteImprove which provides ADA prompts, along with other features. We have to remember to add alternative text to graphics to keep them aligned with TTY expectations.

-

We also use Site Improve. Our sites are hosted by RichWeb in Ashland, VA and they do not have any additional ADA monitoring built in to our plan.

-

Question (8/16/21): With the uptick in COVID cases, what is your bank’s current mask policy for vaccinated and unvaccinated employees?

- Currently masks are highly recommended for both vaccinated and unvaccinated.

-

All unvaccinated public facing employees are to wear masks. However, masks are not required for vaccinated employees & strongly encouraged for unvaccinated.

- Currently, masks are optional for vaccinated employees and required for unvaccinated employees. Our plexi shields are still in place with hand sanitizer stations still present.

- We reinstituted the mask mandate 2 weeks ago. Unless in an office with a closed door, masks must be worn – vaccinated or unvaccinated. We are in talks with management about requiring vaccinations for all employees.

-

Our mask protocol is back in place, unvaccinated wear a mask at all times. Vaccinated individuals wear one if unable to social distance or in a meeting

-

We have the same protocol. As of today, we have returned to having everyone wear a mask in common areas, regardless of vaccination status. We are also required to check in on the ProtectWell app and limit in-person meetings.

-

MASK REQUIRED

Unvaccinated

- All public spaces

- All meetings & gatherings

- All workplace events

- Everywhere except alone in your office or cubicle

- Walking into the building to your desk

- Going from your desk to another part of the building

Vaccinated

- In meetings with others when social distancing of at least 6 feet is not possible

MASK OPTIONAL

Unvaccinated

- Alone in your office or cubicle

Vaccinated

- Everywhere except in meetings with others when social distancing of at least 6 feet is not possible

Question (9/16/21): What are your go-to stock photography services? We have been using iStock but have not been enthusiastic about their offerings.

We focus on the free sites: Pexels, Unsplash, and Pixabay. We do use the others as a last resort!

WARNING TO ALL: We used the free sites and someone filed a lawsuit against us. We settled, but now we only use Shutterstock. It was a huge headache because we had to go through our blog, social, and site to remove anything from Pixabay due to this.

We use Shutterstock.

We use shutter stock and istock and we do a photoshoot every year to have our own personal library

Question (10/7/21): We have a position titled “community development officer”, whose job includes reaching out to the underserved in our community to see how our bank can help both businesses and individuals and assisting our bank in accessing opportunities for diversity and inclusion both internally and in our community. This role is still evolving. Is anyone willing to share job descriptions of any related position(s) you may have in your bank?

We appointed one of our bankers to the role of Community Financial Engagement Officer in 2019. In January 2020, we created the role of Diversity and Inclusion Officer, which is an HR position and looks more to ensure that our internal culture is supporting our DEI goals. I have attached the statement that we share regarding these goals and our activity to support them.

Question (10/15/21): Can I pose the million dollar question – how do you determine your digital marketing budgets?

Our digital marketing currently accounts for about 45-50% of our budget. We try to keep our channels proportionate to the demographics of the areas we serve and utilize what best reaches targeted audiences. Fortunately for us, our executive team is very supportive of our efforts and recognizes that unforeseen circumstances can require an alteration of even the best laid plans. If the past year-and-a-half has taught us anything, it’s flexibility and versatility.

Question (11/2/21): For those of you that hold regular update meetings with your CEO what do you call them? What topics are typically covered?

Our CEO has quarterly Department Head meetings to update us on things to which we may not all have been privy. Additionally, my immediate supervisor and I have Monthly Marketing Updates to check in on projects in production, brainstorm, and – in general – ensure Marketing is on top of what the bank needs.

I meet with our CEO every two weeks. We simply call them 1:1s. It’s pretty informal. I let him know what we are working on that is about to drop so he has no surprises and we talk though anything I’d like his input on. He in turn lets me know about any corporate activities that I may not know about and gets my input as appropriate (sometimes I just offer it anyway J ) and he shares things that he has come across in meetings and his readings that I might find interesting or that he would like for me to explore.

Question (11/23/21): We are redesigning our website and I am evaluating whether or not to switch to .bank and would like to know if any of our committee members have done so – what are the pros and any cons?

Dot-bank is the move. Because there is a vetting and verification process, “.bank” is as good as a blue check mark on a celebrity twitter account (still waiting for my blue check… and to be famous… and to make a twitter in the first place). Cybercrime and cyberterrorism are not going anywhere, and by volume and intensity, it will only get worse. Having that extra level of legitimacy and visual trust can save a lot of dough for us as institutions and clients who may otherwise be hoodwinked and/or bamboozled. Hoping to make the leap to dot-bank soon, too.

One hesitation on our part with the move to .bank is the “speed bump” it creates to log in to online banking, or any external link. The online banking site is a different domain hosted by our vendor. The user gets a message that they are leaving our secure site to go to the online banking site. The .bank set-up may now allow for a more seamless experience when leaving your domain, and if so, I’d love to hear it!

We have had the .bank for 3 years and I think it is advantageous overall. I agree with Josh that it provides a level of assurance. We have also folks who find it confusing, but they are far and few between

We purchased a few dot bank related domains to our name a while back but have not made the move to switch over yet. Interested to hear more thoughts from the committee here too. As far as the speed bumps we follow that setup for external links that aren’t a paid service. For our online banking and ClickSwitch we don’t have speed bumps set up however we do for links to our social media pages, etc.

We’ve had the .bank for a few years now and I agree that it is advantageous from a peace of mind standpoint. We do get the occasional confused look when we audibly direct people to yourbank.bank, but I think that’s more so the repetitive “bank” in the address. We don’t have speed bumps for online banking.

We are planning to make the switch to dot bank with our new website next year.

We made the switch in 2019—at the same time as our online banking conversion. It has been great for all the reasons already expressed. We did a lot of communication to clients/staff leading up to the change so it went very smoothly! Happy to discuss further off-line if there is any specific information folks are looking for.

We reserved a few .bank URLS back in the day when this first opened, we have not utilized the .bank and have no plans in the near future to do so but we are keeping the .bank URLS that we purchased.

I will warn that while we enjoyed .bank at TFB, with the merger, it has caused a giant headache for getting links redirected. Once you have it, they make it hard to let it go. We are months into the official system conversion and still have projects delayed because of .bank.

Question (12/14/21): How much of your marketing budget – in dollars and/or percentage of budget is allocated to sponsorships and/or contributions?

As for donations budget: We dedicate a set amount to branch budgets for local events/projects with another set amount for corporate (impacts throughout our footprint) plus $10,000 for Community Commitment scholarships (ten $1,000 scholarships) for high school seniors headed to four-year college, community college, or licensed trade school.

We are similar in that we have individual branch budgets for sponsorships and contributions. Our sponsorships are carry a large portion of our overall marketing budget around 30% and contributions around 15%. For scholarships we offer 8 individual $2,500 scholarships totaling $20,000 and is included in our contributions percentage. We also have an employee fundraiser for $5 Jeans Fridays in which we utilize funds throughout the year to support other community needs.

Question (1/6/22): As you think about your social media, what channels are you using primarily for your strategy? We are trying to determine the level of effort needed for each channel and are at a cross roads.

We use Facebook and Instagram primarily and LinkedIn when the message is appropriate for that audience. We have not used Twitter because of its reputation as a cesspool full of misinformation. (Even more so that Facebook) We do have a YouTube channel but I don’t anticipate posting on TikTok as of yet. It does appear to be a fun, creative outlet. Feeding that channel fresh engaging content on a weekly basis would be a challenge. (I just don’t have the dancing chops needed!)

We primarily use LinkedIn and Facebook. We have a Twitter account but don’t really get much activity on that so we use it occasionally… ongoing discussion as to whether to just jump off of it. We use Facebook to reach a broad audience, connect with community groups, announce programs and projects, etc. We get a lot of activity on FB from our own people and loyal customers. We used paid FB for promoting products. We use LinkedIn for more business-oriented promotion. We’re working with team members to get them more active on their personal accounts. We talk about Instagram which I personally feel would be great for reaching a younger audience but we hesitate to add another platform and one that is so visually dependent.

Question (1/13/22): We are currently looking for website development/design vendors to shop for a new website and wondered if the committee could share who they’ve used and pros/cons, successes, etc.

Question (2/16/22): Several – if not all – of y’all may have incorporated text messaging as a method for communication with your customers. Will you, please, share with me for what purposes your institution utilizes SMS text?

- We just had a call last week with a vendor, however, so we are considering it. We have a platform we use for SMS communications internally but not externally.

- VNB does not currently use text for communication.

- our bank utilizes text messaging for fraud alerts.

- National Capital Bank is not using text messaging communication with customers.

- We do not currently use text messaging but we are considering it.

- Fraud alerts and online banking alerts

Question (2/25/2022): What is your bank’s current stance on tattoos and piercings in the workforce? What guidelines regarding piercings and jewelry are currently in place?

- Men may not wear earrings. Women may not wear more than two earrings per ear, appropriate for business and only on the ear lobe. No employee may report to work with pierced eyelids, nose, lips, tongues or other body part except as mentioned above. Tattoos may be visible if they are minimum in number, moderate in size, below the neckline and non-offensive. Management reserves the right to approve/not approve exposed tattoos that are inappropriate for a professional business setting.

-

“The company recognizes that personal appearance is an important element of self-expression and strives not to control or dictate appropriate employee appearance, specifically with regard to jewelry or tattoos worn as a matter of personal choice. In keeping with this approach, First Bank allows reasonable self-expression through personal appearance, unless a) it conflicts with an employee’s ability to perform his or her position effectively or with his or her specific work environment, or b) it is regarded as offensive or harassing toward co-workers or others with whom First Bank conducts business and has contact with employees.

First Bank permits employees to wear jewelry or to display tattoos at the workplace within the following guidelines. Factors that management will consider to determine whether jewelry or tattoos may pose a conflict with the employee’s job or work environment include: 1. Personal safety of self or others, or damage to company property. 2. Productivity or performance expectations. 3. Offensiveness to co-workers, customers, vendors or others in the workplace based on racial, sexual, religious, ethnic, or other characteristics or attributes of a sensitive or legally protected nature. 4. Corporate or societal norms. 5. Customer complaints. If management determines an employee’s jewelry or tattoos may present such a conflict, the employee will be encouraged to identify appropriate options, such as removal of excess or offensive jewelry, covering of tattoos, transfer to an alternative position, or other reasonable means to resolve the conflict. The employee will be given five (5) business days to remedy the issue.”

-

Visible body piercings must be limited to earrings (small to moderately sized and no more than two per ear) and small nose studs (no septum and rings)

Tattoos are allowable (except on throat or face) unless excessively distracting, inappropriate or offensive

The policy is under review now and we are planning more flexibility with facial piercings.

-

We use to say ALL tats had to be covered and no piecing’s other than ears but the last 3 years we have gotten a lot more hip and now the entire body can be tattooed up but nothing vulgar or offensive can be visible .

-

Tattoos related to all Employees: Tattoos should be limited, not visible on the face or neck, should be of good taste and not obscene or offensive. Half or full-sleeve tattoos must be covered at all times. Management reserves the right to require an employee to cover tattoos dependent on the business situation.

Piercings related to Women:

Items not permitted: More than two pierced earrings per ear, ear gauges, other visible body piercings,…

Piercings related to Men:

Items not permitted: earrings, ear gauges, visible body piercings,… -

Our policy says that face piercings and visible tattoos are prohibited. (The tattoo portion may be under review though, as I’ve seen them on employees and they don’t appear to have an issue with them as long as they’re minimal and non-offensive.)

-

Dress Code: In order to service a growing and diverse client base that covers multiple regions, employees are required to dress in appropriate business professional attire that is clean, free of holes, tears, or other signs of wear. No clothing should be worn that may create a safety hazard. Additionally, employees must cover exposed tattoos or body piercings, when possible. Clothing or grooming styles dictated by religion or historically associated with race or ethnicity are exempt from this policy.

-

Here’s the section of our professional appearance policy that deals with piercings and tattoos:

All articles of clothing must be clean and pressed neatly, and employees must be well-groomed. Employees must refrain from wearing excessive jewelry. Facial jewelry, such as tongue, eyebrow, and nose rings are not acceptable to be worn during working hours or while representing the Bank. Hair styles and colors must be professional and not extreme. While conducting Bank business, any visible tattoo(s) should be minimal and must not be of an offensive nature.

- Men may not wear earrings. Women may not wear more than two earrings per ear, appropriate for business and only on the ear lobe. No employee may report to work with pierced eyelids, nose, lips, tongues or other body part except as mentioned above. Tattoos may be visible if they are minimum in number, moderate in size, below the neckline and non-offensive. Management reserves the right to approve/not approve exposed tattoos that are inappropriate for a professional business setting.

Question 3/21/22: If your bank offers online account opening, how do you ask applicants risk-rating type questions, such as will you send or receive wires over a certain amount; will you send or receive wires from non-US locations; do you have citizenship with another country, etc.? Are these built into your online account opening solution? Or are you following up with those applicants via phone or email?

- We are developing an Online Account Opening form on our new website to gather initial information and our New Accounts Team will follow-up with the client. At that time I would think they would inquire about wires, etc. Our idea was to start with this form and gauge interest before looking to vendor solutions. We previously had Online Account Opening when we were with FIS but, found it very costly and the accounts opened via this channel tended to be unfavorable accounts.

-

We are launching our new online account opening tool next week. We decided to go with a packaged solution because of the additional layers of id verification and fraud prevention built into them. We vetted a few different vendors and chose to go with a solution by Newgen.

March 2022: We would like to begin using Google Tag Manager and understand there are compliance/disclosure guidelines to follow such as having a separate disclosure for we website privacy, how cookies are used for advertising and how analytics help to better understand website visitor. Do you have separate disclosures, an acknowledgement of cookies and any other privacy statements on your websites, if so would you mind sharing?

We have drafted and updated our digital use practices throughout the years. Here is the current language on our public website: https://www.townebank.com/privacy-and-security/digital-use-agreement/

March 2022: Looking at SEO spend for our bank and wondered how other banks price their budgets? How do you determine how much you allocate?

April 2022: Our Security Department is concerned about a rise in theft of checks out of US Postal Boxes and have asked us to develop a campaign to alert/educate our customers. Have any of you had to address this issue? If so, what did you do and do you know if it was effective?

So, it wasn’t for this issue specifically, but with rising cybersecurity threats, our IT department asked us to publish a list of tips they worked on in conjunction with Zelle to inform our customers of ways to prevent falling victim to a scam. We posted the tips across our social media platforms. There really isn’t a way to gauge the effectiveness of this, other than looking at interactions on the posts and engagements to see if the information is reaching them. It doesn’t hurt to put the information out there. It makes it accessible to those who use social media frequently and sometimes that is far more effective than printing it on statements or publishing it to your website.

For any of us that use Banzai’s FinEd platform, they recently launched a series dedicated to security. Our Digital Marketing Manager (also a member of this august group) shares their social media posts linking to the various topics they address in any given month. Great stuff!

April 2022: I have a question about Works24. I’m wondering if banks who use this vendor for overhead music and lobby video are happy with them and if they don’t use this vendor who do they use and do they like them.

We use them for branch video monitors and they have been great to work with. Wanted to clarify that although we use Works 24 we don’t use their pre-made slides or video, we create our own. You can also upload any TV commercials or website video to the Works 24 players. We also encourage branches to advertise community events. We do a business of the month and showcase a local business customer and they love it!

We switched to Works24 last year for lobby video and the on hold phone messaging service and are extremely happy with them. The process to get set up was so easy and their customer service is very responsive. The solution is very user-friendly. We left InLighten where everything was a challenge.

We use them and are generally happy with the service. Tance, who handles this for us, reports that the customer service is very good – her only wish is that they had updated content more often.

We are just now renewing a 3yr agreement with Work24. (Video and Audio) They have a lot of content that requires curating, but there is enough variety to keep the feed fresh from month to month. I have been especially impressed with their after sales service. It is exceptional.

We are entering our fifth year with them and truly appreciate their responsiveness and the ease of facilitation. The biggest challenge for us sometimes is that the vultures holding up the phone lines between poles take way too many smoke breaks, but that is one of the beauties of rural Southside Virginia. We upload radio (on hold messaging) and video spots to Works24. It integrates quite nicely.

We use them for on-hold and video only in a couple branches and are generally happy with them. My only issue is that I don’t love the two options for voice talent. I bit over the top in my opinion but easy enough to do your own or hire out.

May 2022: Who do you use for digital asset management? We have been looking at Bynder and Box. Does anyone currently use either and/or do you have any services to suggest?

Farmers Bank does not currently use a digital asset management vendor.

Benchmark hasn’t tackled an outside vendor for digital asset management.

Burke & Herbert Bank is not using a digital asset management vendor.

National Capital Bank – Not currently using one. “We keep all our “photos” in DropBox that we share a log in with our agency. Not ideal so would love to learn more digital asset management.”

Atlantic Union Bank – “We recently started using Bynder too soon to know if it is worth the investment.”

American National Bank & Trust - We store our photos on our internal drive – not a great system but our library isn’t enough to invest in a DAM.

Old Point National Bank – “We do not currently use a DAM. We do most things in-house and have a small team so we just try to keep a well-organized shared drive. We use Dropbox when we need to share resources externally.”

TowneBank - We have had Box for years, mostly as a file transfer service for large files or to send material to outside vendors, auditors, etc. We are now on Bynder for our website library and hopefully to provide some custom templates to our business development teams who are spread across two states. We also are cataloging professional images of our bankers and executives and other photography that we format for multiple uses – social media, newsletter, website, collateral, etc. I’m happy to connect anyone to our project manager who is setting up our asset library.

Village Bank - At Village Bank we also currently use an internal folder system vs a DAM, much to my chagrin. Having managed the implementation of a DAM solution and a Library Archive system for a global organization I am all too familiar with the effort and expense that goes into not just setting it up but also, and possibly more importantly, what it takes to manage and maintain. As such, if we do decide to go that route, I will likely look at open-source solutions first. Here are a couple of other unsolicited quick tips I can offer from experience: try to avoid customizations as they will likely become wrenches in the system later on down the road; your assets are only as good as their metadata so invest the time necessary to thoroughly complete the tagging process.

May 2022: Is your bank currently looking to change or has it changed its overdraft/NSF practices in light of regulatory scrutiny? If so, what has changed?

Farmers Bank hasn’t changed overdraft/NSF practices yet but, we are closely monitoring all angles.

Benchmark has not changed overdraft/NSF practices.

Burke & Herbert Bank has not.

National Capital Bank has not.

American National Bank & Trust – “We will be making some changes to our NSF/OD program later this year to be more consumer-friendly.”

Old Point National Bank – “We are currently reviewing our overdraft fees and considering some updates, but haven’t made any changes yet.”

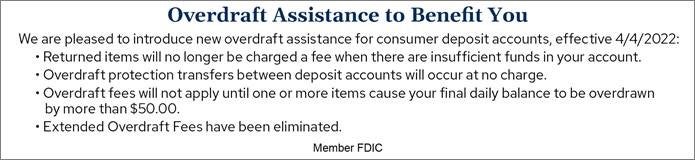

TowneBank - We made significant changes to personal OD/NSF practices, effective 4/4/2022. The second bullet about removing transfer fees also applies to business accounts. This was our statement message on personal accounts: TowneBank Statement.

{kind=link}

Village Bank - As of June 1st we will be eliminating our Overdraft Assurance.

May 2022: Is your bank a Bank On certified bank or working to become one?

Farmers Bank is working to become a BankOn bank. We have received interest from a few area non-profits and plan to start with a test environment assisting these organizations to see how it goes before offering it fully.

Benchmark is not a Bank On certified bank. I haven’t heard anything about that road being traveled as yet.

Burke & Herbert Bank is not.

National Capital Bank is not.

American National Bank & Trust – “We are interested in being a Bank On certified bank but have not yet started the process.”

Old Point National Bank – “We are also considering adding a Bank On certified or similar account.”

TowneBank - We have been a Bank On partner in several cities, but we do not offer the matched savings accounts at this time.

Village Bank - We are not Bank On certified but it is a direction we will be looking at in the coming couple years.

May 2022: Does your bank utilize Q2?

-Old Point National Bank, Village Bank, Freedom Bank and Chesapeake Bank

May 2022: How is your bank celebrating or acknowledging Juneteenth this year?

Closed: Burke & Herbert Bank, C&F Bank, Benchmark Community Bank, First National Bank, VBA, Virginia National Bank, TruPoint Bank, Village Bank

First Bank, Virginia:

“For Juneteenth, this will be the second year we host a celebratory picnic with games, music, face painting, etc. at Fremont Street Nursery (previously named the Negro Day Center, opened in 1943).

Here is an article from last year’s event, for those interested.

We’re also sponsoring & setting up a booth at the Winchester NAACP’s Juneteenth Celebration on Sunday.”

Old Point National Bank:

“We have planned social media posts and an internal message to our employees. We are also sponsoring and attending a couple local festivals being held in celebration Juneteenth, like the Hampton African American Heritage Festival.”

American National Bank & Trust:

“We are closed in observance and also have some communications developed for both internal and external audiences.”

May 2022: Does your bank have a volunteer policy? We’re looking at designing a program to encourage volunteering in situations that may yield CRA credit. I’d love to hear if anyone else has one and if they are willing to share their description/policy etc.

At National Capital Bank, we don’t have a formal policy, but strongly encourage all employees to volunteer their time, talent or treasure, especially those in customer-facing positions – branch team members, loan officers, business development, etc. as it’s really part of their responsibility to be involved in the community. We track charitable organization involvement as well board membership with chambers and leadership orgs, committee work, event planning- the committee counts towards my hours. But we don’t have a set number of hours per employee. We survey each year which helps us with reporting on our CRA exam as well as for other promotional reasons.

Village Bank:

We do not have a Board Policy but paid volunteer time is included in our Employee Handbook as a benefit:

Volunteer Days

The Bank is committed to making our community strong by improving the places where we work and live. The Bank encourages all employees to give back to their communities by participating in the Volunteer Day Program. All full-time, regular employees have the opportunity to use up to 2 paid workdays each calendar year to volunteer for a recognized, community non-profit cause or organization, with their supervisor’s prior approval. Volunteer days cannot be accrued or accumulated and may not be used by new employees until they have completed 90 days of continuous employment. Part-time employees who work less than 30 hours per week and seasonal, temporary employees (both full-time and part-time), and fully commissioned loan officers are not eligible for volunteer days. Eligible employees must submit a Volunteer Request Form to their supervisor at least 30 days prior to the date requested to be used as a volunteer day(s). The employee’s supervisor and the Human Resources Department must approve the Volunteer Request Form, including the recipient non-profit cause or organization. Volunteer days may be used consecutively and prior to or following a weekend and in hourly increments. Employees are requested to identify themselves as Bank employees while participating in volunteer days by wearing Bank logo wear whenever possible.

I also have Stephen, our Community Engagement Manager, actively trying to drive greater utilization of this benefit. What we have seen is very few hours formally submitted but we know that volunteer hours are much higher than that metric suggests.

American National Bank & Trust: We encourage volunteerism and also really try to track it. We are working towards an annual goal of 1500 hours, which we are about 25% there. American National provides ½ day off per year to volunteer for the community and similar to Chesapeake, they get paid regular salary with no PTO used. There is no formal volunteer policy.

Chesapeake Bank: Chesapeake Bank allows for employees to take two (2) days off a year to volunteer for a good cause in the community. The employee collects their regular salary, and it does not count against them as vacation.

Benchmark Bank: Benchmark also has no formal policy for volunteer activities. Like many of you, we encourage volunteer engagement in our communities. Some of us have taken on enough for three or four people.

To my knowledge, Bank of the James doesn’t have a formal “policy” – we encourage these activities, especially for organizations/events we support, but the structure is basically up to staff and supervisors.

June 2022: Is anyone is doing a Skip-A-Payment program and if so, is it a digital/electronic process versus mailing a letter that the customer has to sign and return in person?

Atlantic Union Bank: We never found the skip a pay program to be successful for our bank and had very little interest from the customer base.

July 2022: Where do you store your videos? Do you use a platform that’s suitable for storage of videos for the bank’s records as well as internal and external distribution (Vimeo, YouTube, etc.)?

First National Bank: So, it depends on what kind of video and what purpose it serves. If it’s a training video to be shared internally, we store on DropBox. If I’m going to embed it somewhere and it’s not confidential, YouTube. Lastly, we do archive all videos on our server.

Burke & Herbert Bank: Currently, we use vimeo but we’re thinking about exploring other options. We haven’t yet shared many videos externally.

C&F Bank: We use Vimeo for our internal video library and YouTube for external content.

February 2023: If you use a service for SEO and google ads, can you share what service you use, and what you like about them?

Old Point National Bank: We don’t use a service for SEO or Google ads currently. We have used a few different third-parties in the past, but I have someone on my team now who is Google ad certified and we are having better results managing this in-house. For our soon to be new website, we’ve chosen a CMS which has some built-in SEO features so we’re hoping to see a jump up when we transition over to the new site.

National Capital Bank: National Capital Bank does not use an SEO service. Our agency helps us in creating Google Ad Search campaigns. We just launched our new website, so we are still working through the process of updating as we go along.

February 2023: Does your bank identify the VBA Bank Day Scholarship Program and/or Virginia Reads One Book on your CRA report? If yes, have these programs qualified in the past?

National Capital Bank: has not participated in the Bank Day Scholarship program, but we did join in for VAROB last year and I believe it was reported on our CRA report for financial literacy working with a Title One school.

March 2023: Do any of you have to deal with Facebook comments/reviews like the samples below? We have been seeing these pop up fairly regularly. It’s obviously phishing, but we are hesitant to get into the practice of removing reviews. We usually post a disclaimer and reminder for customers to be careful to not fall for scams. If you do receive them, how do you handle them?

- As they are not real and may cause damage to the client, we delete or hide the comments on social media.

-

We haven’t gotten too many of these either, but I would feel comfortable just removing them since they are not legitimate reviews. In fact, our very dedicated IT and Compliance departments would most likely feel better about removing these fraudulent phishing “reviews.” Even publishing a statement warning customers about such threats may not be enough to prevent people from falling for this scam. It’s probably best to just eliminate the threat altogether and ensure customer protection.

-

We had a period where we got quite a bit of these reviews. We deleted them since they were phishing and not a legit review. We also occasionally get comments with the same content, that we delete as well. We don’t want our media channels feeling fake or scammy.

-

Same as above. Since these are not legitimate reviews/comments we do not feel bad about removing them. We haven’t really gotten that many – thank goodness!

-

We haven’t received as many, but we do delete as well. I agree with the comment below. That’s our take on it.

-

We do receive these messages from time to time and I delete them. They are phishing messages, not legitimate or a review, so I don’t think you need to worry about any backlash from deleting them. We also get comments saying, “promote on…a certain site” and I also delete those.

-

Well, this is a very interesting question indeed! I don’t think we’ve received many of these, but I’m not the first point of contact to review so I’m going to do a little research. I agree with you guys though – slippery slope to think about removing BUT not a great reflection to keep something up that is so shady-feeling! Thanks for raising the topic.

-

Hi I do the same. I just delete them if they seem sketchy or spam/phishing.

-

We have been getting a lot of these type of reviews and comments too. We delete the comments because they are obviously spam, but you can’t delete or hide a review/recommendation. We were commenting on each one saying that this review is not legitimate to try to protect people from falling victim to them and then reporting them, but Facebook never removed any of them. Our reviews section was getting so overrun with them that we decided to hide our reviews section on Facebook until we can hopefully get past this phase.

Looking for an example of a marketing policy to use internally. Does anyone have examples they can share?

Does anyone have any experience working with inLighten, an on-hold & video message marketing company? If so, I’d love to hear what you have to say about them and their product. We currently use Works24.

- Atlantic Union Bank: We moved away from Works 24 as of July 1; they were great to work with but they were having trouble getting in new equipment that they had been promising us for 5 years and the old stuff was breaking. We decided to take our monitor ads in house; if you can hook up zoom players to your TVs you can do it yourself. This saved us $110,000 a year.

- Pendleton Community Bank: I talked with both Works 24 & inLighten as an alternative to a provider we weren’t pleased with. Both pricing and product were fairly similar. We ultimately decided to also bring it in house and saved a ton of money per year.

- Freedom Bank: Hi everyone! We used to work with inLighten but stopped about 4 years ago and brought it in house. They were fine to work with, but we realized we could do it ourselves and save the money.

- Bank of the James: Same – we’ve just dramatically reduced our W24 contract (branch tv content) but are still using them in 2 branches and for phone voiceover. I’ve had a real issue with cold calls from Inlighten – same person leaves message after message and says that “fill in the blank executive” (names our COO or someone similar) told her to reach out to me. I go to that executive and discover no such referral was made. I have stopped returning her calls because even after I explain this and say we’re happy with our vendor, she continues to make the same attempt. Doesn’t lead me to want to give her our business if that makes sense.

Who do you use for your board portal? What is the level of ease to use it and your satisfaction with it?

- Old Point National Bank: I believe we use Groupsite for our board portal. I haven’t heard any complaints about it, but I’m not very involved as I don’t have to help manage our board relations/communications anymore.

- No board portal for Bank of the James

- Freedom Bank: We use Onboard for our board portal. I have heard good things about it but our power user is our executive assistant so she would know much better than I do how it is on the backend.

Who is offering CD promotions and also how are you marketing your deposit promotions? [Traditional advertising vs all digital marketing.]

- Bank of the James: We started some CD promotions last spring and marketed them in print ads, in-branch signage and direct outreach. It went very well and accomplished what we set out to do – grow deposits!

- Atlantic Union Bank: CD Promotions have been 100% digital for us with mass media outside of the branch as it allows us to quickly adjust due to rate changes. In branch we do post CD special. No print advertising. Our results have met expectations.

- Old Point National Bank: We have a few different CD specials and a money market special. We are advertising across a mix of traditional and digital channels (in branch, print, email, paid digital, social media, etc.). We even did some digital billboards over the summer.

- Freedom Bank: We are running a 12-month promo CD right now that we are promoting through print (three different publications) and digital.

What resource do you use to aggregate, manage and schedule your social media posts (Planoly, Hootsuite, etc)? How do you find the user experience/what is your level of satisfaction with it?

-

Oak View National Bank: I use Sprout Social, and it works great for our needs. I would highly recommend it!

-

Virginia National Bank: We use Hootsuite. Easy to use platform, but we are not super active on social media at this time.

-

Old Point National Bank: We’re using Hootsuite, but the pricing keeps going up so we’re interested in seeing if there are any other better priced options out there. Looking forward to everyone’s feedback.

-

Benchmark Community Bank: Good afternoon! When Hootsuite was free, we used that service to manage Facebook, LinkedIn, and Instagram. Overall, it was great for me. One feature I really liked was being able to assign the photo/image I uploaded to a photo album within the scheduled Facebook post. The only snags came from uploading videos because there was a file size limit. Once Hootsuite switched to paid plans only, we searched for other options and landed on Buffer, which was reasonably priced for us. We’re no longer able to select a photo album during scheduling, but Buffer works very well in managing our three channels. Rescheduling a post to another day on the calendar is easy with a drag-and-drop feature. I’m quite satisfied with Buffer, but I’d love to hear what other solutions are out there. Thanks for asking this question!

-

Powell Valley National Bank: We’ve been using Buffer as well and have been satisfied with it.

-

Village Bank: I asked Bridget Minner to provide a response to the question: “Meltwater is one of the better social media tools I’ve worked with. It offers the basics and more, and the analytics dashboards have been super useful. Not to mention, I’ve really valued the AI copywriting features they’re offering using CHAT GPT. I will add that the interface itself can be glitchy, and certain functions (ex: scheduling Instagram stories) have never worked well for me. For the most though, it has never stopped me from knocking out everything I need to and then some. It is very easy to learn this tool quickly.” Mind you Meltwater is not inexpensive but the social media tool is just part of a larger package that we have with Meltwater. We also use them for Media monitoring, social listening and the distribution of an occasional press release in addition to our social media management tool. We also have calls with our assigned account manager every other week and they will do basically anything we ask them to help us with, especially in refining our reporting.

Does anyone use text messaging for marketing, and if so, what program/app do you use?

Old Point National Bank: We use a platform called Digital Onboarding that sends out marketing messages via email and text to our customers. Currently, we are just using the platform for communicating with new customers to welcome them and encourage them to activate their debit card, sign up for direct deposit, etc., but it can also be used for other marketing purposes like cross-selling.

Benchmark Community Bank: We don’t use it for marketing products and services, though use the SMS Text feature on SimplyCast for operational notices such as inclement weather, power outage, etc. impact. We can send by market. Thanks!

Do your boards allocate your marketing budgets based on your asset size? For example, they allocate 1% of asset size for marketing ($500,000 budget for a bank with an asset size of $5 million). Or just in general, how would your budgets compare to your asset sizes?

No responses.

The Bank’s marketing officer includes the NMLS number on all advertisements regarding consumer mortgage loans. However, advertisements not associated with consumer mortgage loans do not include the NMLS number of the loan officer as per our understanding of the law. An outside auditor is stating we should include the loan officer NMLS number on EVERYTHING. Curious to what others are doing?

Burke & Herbert Bank: We only include the NMLS# on mortgage related materials and advertisements.

Powell Valley National Bank: Same here, we only include it on mortgage related materials.

Oak View National Bank: We only include NMLS on mortgage related materials, and on their business cards.

F&M Bank: That’s interesting, I’ve never had an auditor question that before. We include the NMLS# on anything credit-related (mortgage, consumer lending, and credit card). Unless there has been a change to regs I haven’t seen yet, I would suspect the outside auditor’s recommendation must mean your audit is otherwise going very well and they have to give you a best practice on SOMETHING!

Virginia National Bank: Same—we have only included NMLS on targeted marketing materials (e.g., a lender is featured), business cards, website, and signature lines.

First Bank, Virginia: Same as everyone else! We only include the lender’s NMLS on mortgage related material, business cards, website and signature lines. On our generic marketing material, where no lender is featured, our internal compliance officer has us include the Bank’s NMLS #.

Bank of Botetourt: Our practices regarding compliance are the same as others have mentioned.

Atlantic Union Bank: Likewise for us.

Freedom Bank of Virginia: The same for Freedom!

Bank of the James: Exact same for BOTJ!

Village Bank: Ditto for Village Bank

Benchmark Community Bank: Great question! Our Compliance department wants us to put the MemberFDIC and Equal Housing Lender logos on all ads. The NMLS numbers for the bank and any referenced lenders are included on mortgage/lending ads. However, we don’t include the NMLS number on non-lending ads.

Old Point National Bank: We include the lender’s NMLS # on their business cards, website, and signature lines. On personalized lending related marketing materials, we include the lender’s NMLS # and the Bank’s NMLS #. On our generic lending marketing materials, we just include the Bank’s NMLS #. We don’t use any NMLS information on marketing materials that aren’t related to lending.

Does anyone have a mystery shopper form they use for their employees to shop their local competition? We are trying to make sure our employees know what other banks in our area offer – including their fees, but we also want them to be more knowledgeable about services and products we offer and our fees in the process.

Virginia National Bank: VNB does not currently ask employees to shop local competitors. We do have employees that provide mailers to management to keep us all informed.